The money supply includes more than just coins and paper money. In fact, checking account deposits are the most common form of money in the United States and many other countries. In the United States, about three—fourths of all payments are made by check. Checks are a safe and convenient medium of exchange. In addition, a canceled check provides written proof that payment was made.

Economists define the money supply in various ways, depending on which assets they include in their measurements. The definitions change as the banking system changes. Two major definitions of the U.S. money supply are called M-1 and M-2.

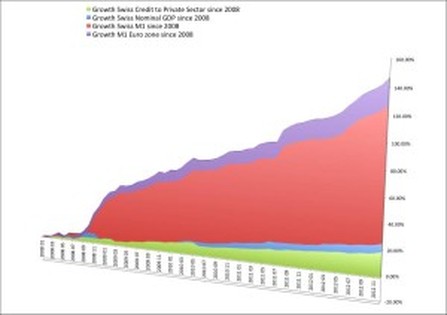

M-1 consist of checking account deposits, also called demand deposits; traveler’s checks; and currency. In the mid-1990’s, M-1 totaled about $1,125 billion.

M-2 consists of M-1 plus money invested in savings accounts at commercial banks, at savings banks, and at savings and loan associations. Such savings, called time deposits, are not immediately available to make purchases. The saver first has to withdraw the money, and the bank can require advance notice of withdrawal. However, most people can easily convert their savings to cash or checking deposits. M-2 amounted to about $3,560 billion in the mid-1990’s.

Economists define the money supply in various ways, depending on which assets they include in their measurements. The definitions change as the banking system changes. Two major definitions of the U.S. money supply are called M-1 and M-2.

M-1 consist of checking account deposits, also called demand deposits; traveler’s checks; and currency. In the mid-1990’s, M-1 totaled about $1,125 billion.

M-2 consists of M-1 plus money invested in savings accounts at commercial banks, at savings banks, and at savings and loan associations. Such savings, called time deposits, are not immediately available to make purchases. The saver first has to withdraw the money, and the bank can require advance notice of withdrawal. However, most people can easily convert their savings to cash or checking deposits. M-2 amounted to about $3,560 billion in the mid-1990’s.

RSS Feed

RSS Feed